[lwptoc]

The Federal Budget 2021–22 was handed down at 7.30 AEST pm on Tuesday, 11 May 2021. TaxBanter’s Federal Budget Summary and Federal Budget Quick Reference Timeline can be downloaded for free from our website.

One of the key tax measures is a long-anticipated proposal to change the tax residency tests for individuals to better reflect the modern world. This article outlines the Board of Taxation recommendations which underpin the Budget measure and sets out the model on which the new rules will likely be based.

This article also briefly outlines other Budget proposals to update tax residency tests for other entity types — trusts, corporate limited partnerships and superannuation funds.

Australia’s current tax residency rules for individuals are difficult to apply in practice, creating uncertainty and resulting in high compliance costs for individuals and their employers — including the need to seek third-party advice, despite having otherwise simple tax affairs.

In May 2016, the Board of Taxation (the Board) commenced a self-initiated review of the current individual tax residency. In August 2017 the Board presented its findings to Government in its report titled Review of the Income Tax Residency Rules for Individuals (the 2017 Report).

The Board concluded that the current individual tax residency rules are no longer appropriate and require modernisation and simplification. In particular, the current rules do not reflect global work practices, and impose an inappropriate compliance burden on many taxpayers in all but the simplest of cases — this has led to increased uncertainty and disputes. In addition, the Board identified a number of integrity concerns that arise due to the way in which the current rules operate.

Some of the Board’s key observations are:

The Board recommended that the Government replace the current rules with an improved and simplified residency test based on a ‘two-step’ model — a simple bright-line test followed by a more detailed analysis in more complex cases.

Before taking a position on the 2017 Report, the Government asked the Board to undertake further consultation on its key recommendations. The Board undertook consultation in late 2018. The Board released its report titled Review of the Income Tax Residency Rules for Individuals: Consultation Guide in September 2018 (2018 Consultation Guide), outlining a series of design principles aimed at developing new residency rules, with a particular focus on the following:

After further consultation, the Board submitted its final report to Government titled Reforming individual tax residency rules — a model for modernisation (the Final Report) in March 2019 in which it set out a model for simplifying and modernising the current individual residency rules.

The Board has developed proposed rules to re-focus tax residency in three critical ways:

The proposed model is intended to:

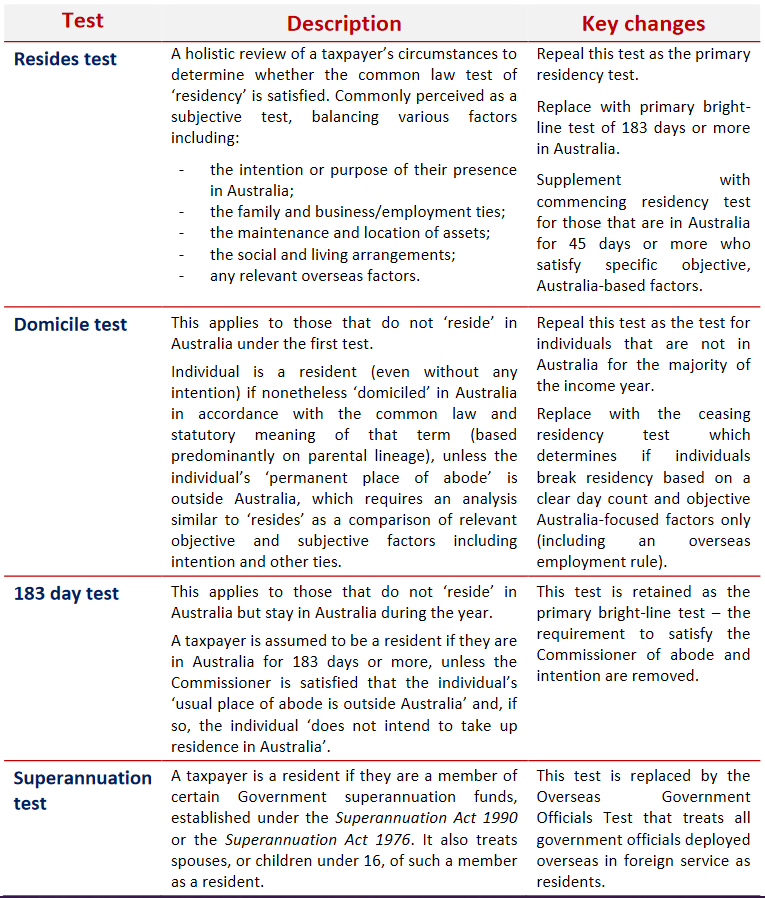

Under current law, the definition of ‘resident or resident of Australia’ in s. 6(1) of the ITAA 1936 includes an individual who is a resident under ordinary concepts as well as an individual who is resident under one of three statutory tests.

The Final Report summarises the four residency tests and the Board’s proposals as follows:

Source: Board of Taxation, Reforming individual tax residency rules —

A model for modernisation, Table 1, page 112

References

References

The ATO fact sheet Your tax residency provides general guidance on the residency tests.

The ATO fact sheet Residency and source of income sets out the ATO’s guidance in relation to individual residency issues which arise as a result of COVID-19 international travel restrictions.

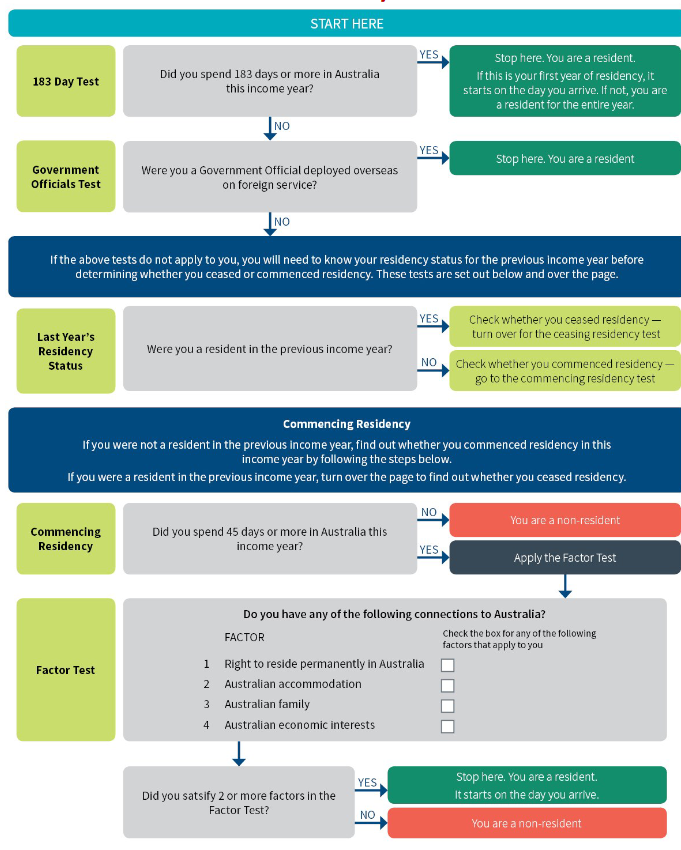

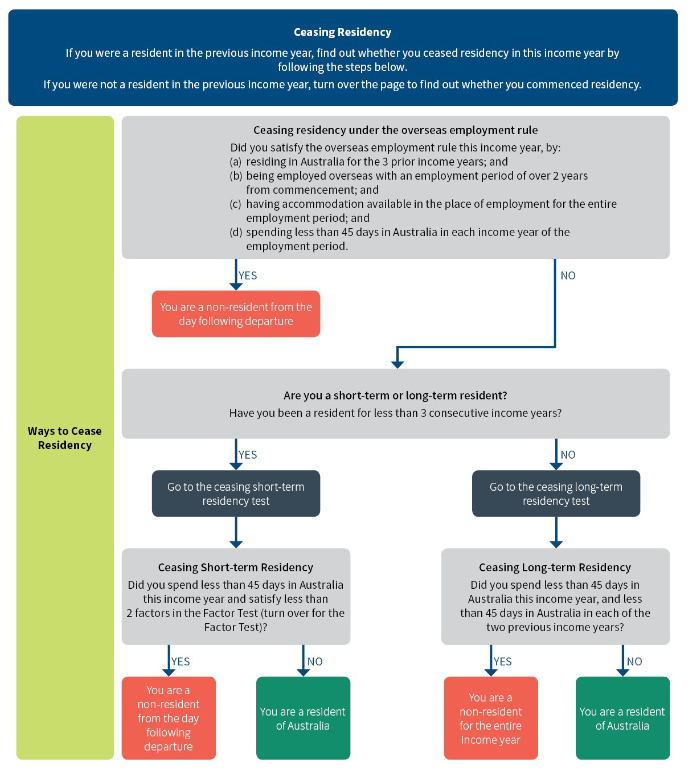

As part of the 2021–22 Federal Budget, the Government announced that it will replace the individual tax residency rules with new primary and secondary tests to determine residency, based on the Board of Taxation’s recommendations.

The primary test will be a simple ‘bright line’ test under which a person who is physically present in Australia for 183 days or more in any income year will be an Australian tax resident.

Individuals who do not meet the primary test will be subject to secondary tests that will depend on a combination of physical presence and measurable, objective criteria.

The new tests are proposed to commence from the first income year after Royal Assent of the enabling legislation.

The Budget papers do not contain any details about the Government’s proposal, but as an indicator of what may be planned, this is the Board’s recommended model:

Source: Board of Taxation, Reforming individual tax residency rules —

A model for modernisation, page 17-18

| Entity | Residency test |

| Company s. 6(1) of the ITAA 1936 |

A company is a resident if:

|

| Trust estate s. 95(2) of the ITAA 1936 |

A trust estate is a resident trust estate in relation to an income year if:

|

| Corporate limited partnership s. 94T of the ITAA 1936 |

A corporate limited partnership (CLP) is a resident if:

|

The corporate residency rules are fundamental to determining a company’s Australian tax liability. The ATO’s interpretation following the High Court’s 2016 decision in the Bywater Investments Ltd v FCT departed from the long-held position on the definition of a corporate resident. As a result, the Government requested the Board of Taxation review the definition in 2019–20.

In Bywater the High Court was required to determine whether a number of foreign companies were residents. The majority confirmed that the test for central management and control has, since its inception, been concerned primarily with identifying the actual location of a company’s central management and control, as opposed to mechanically placing central management and control in the jurisdiction in which a company’s board of directors meet.

TR 2004/15 expressed the ATO’s former view that carrying on business in Australia is a separate requirement of the central management and control test, and one that needs to be established independently of the exercise of central management and control in Australia.

The ATO, in response to the decision, withdrew TR 2004/15 and replaced it with TR 2018/5, in which the ATO expressed its revised view that, to satisfy the central management and control in Australia requirement:

It is not necessary for any part of the actual trading or investment operations of the business of the company to take place in Australia. This is because the central management and control of a business is factually part of carrying on that business.

It is possible under this view that the central management and control test can be satisfied by a foreign incorporated company that carries out operational activities wholly outside Australia.

In the 2020–21 Federal Budget, the Government announced that it would make technical amendments to clarify the corporate tax residency test.

The law will be amended to provide that a company that is incorporated offshore will be treated as an Australian tax resident if it has a ‘significant economic connection to Australia’, which will be satisfied where both the company’s core commercial activities are undertaken in Australia and its central management and control is in Australia.

The proposed change is in line with the Board’s key recommendation in its 2020 report Review of Corporate Tax Residency and will mean the treatment of foreign incorporated companies will reflect the position prior to Bywater.

The amendment is proposed to apply to the first income year after the date of Royal Assent of the enabling legislation, with an option to apply the new law from 15 March 2017. Legislation to give effect to the measure is yet to be introduced.

As part of the 2021–22 Federal Budget, the Government announced it would consult on broadening the amendment to the corporate residency test to trusts and corporate limited partnerships. As per the table above, both of these definitions also include the central management and control test.

The Government will seek industry’s views as part of the consultation on the original corporate residency amendment. The timeframe for the consultation is yet to be announced.

Section 295-95(2) of the ITAA 1997 sets out the requirements for a superannuation fund (including an SMSF) to be an ‘Australian superannuation fund’. Broadly, this is the case if:

The law also contains a safe harbour in s. 295-95(4) under which the central management and control of a superannuation fund is deemed to be in Australia if the central management and control is temporarily outside Australia for a period of not more than two years.

Trustees who were genuinely intended to be temporarily absent from Australia for less than two years may have become stranded overseas because of the COVID-19 crisis, resulting in a forced absence of more than two years. The ATO has provided website guidance that:

If the individual trustees of an SMSF or directors of its corporate trustee are stranded overseas due to COVID-19, in the absence of any other changes in the SMSF or the trustees’ circumstances affecting the other conditions, we will not apply compliance resources to determine whether the SMSF meets the relevant residency conditions.

The Government proposes to ease the residency test by:

This will allow members of these two types of funds to continue to contribute to their superannuation fund whilst temporarily overseas, ensuring parity with members of large APRA-regulated funds.

This measure will have effect from the start of the first income year after Royal Assent of the enabling legislation, which the Government expects to have occurred prior to 1 July 2022.

Join us at the beginning of each month as we review the current tax landscape. Our monthly Online Tax Updates and Public Sessions are excellent and cost effective options to stay on top of your CPD requirements. We present these monthly online, and also offer face-to-face Public Sessions at locations across Australia. Click here to find a location near you.

If you’d like a full rundown of the Federal Government Budget, check out our resources page or listen to our recent Federal Government Budget webinar.

If you’re a current in-house or public session client, you can expect complete coverage of the Budget and how it will affect you and your clients in your next session.

If you’re not a current client, we can also present these Updates at your firm (or through a private online session) with content tailored to your client base – please contact us here to submit an expression of interest or visit our In-house training page for more information.

Our mission is to offer flexible, practical and modern tax training across Australia – you can view all of our services by clicking here.

Join thousands of savvy Australian tax professionals and get our weekly newsletter.