On 12 December 2022, the Treasury Laws Amendment (Electric Car Discount) Bill 2022 was enacted to provide an FBT exemption in respect of eligible electric vehicles. The exemption retrospectively applies to eligible car benefits provided from 1 July 2022.

The objective of the exemption is to encourage a greater take up of electric cars by making them more affordable and to reduce Australia’s carbon emissions from the transport sector. The exemption will be reviewed after three years to consider the electric car take-up. The ATO has indicated the Government will complete a review by mid-2027.

The new s. 8A of the Fringe Benefits Tax (Assessment) Act 1986 provides that a car benefit is an exempt benefit in relation to a year of tax if:

![]() Note

Note

The FBT exemption relates to car fringe benefits and therefore will only apply to vehicles that are ‘cars’ for FBT purposes.

A zero or low emissions vehicle, which is eligible for the FBT exemption, is defined as:

(a) a battery electric vehicle, or

(b) a hydrogen fuel cell electric vehicle, or

(c) a plug-in hybrid electric vehicle.

The legislation sets out the criteria defining each of the three categories of zero or low emission vehicles.

From 1 April 2025, a plug-in hybrid electric vehicle will not be considered a zero or low emissions vehicle under FBT law. However, the exemption will continue to apply if the use of the vehicle was exempt before that date, and there is a financially binding commitment to continue providing private use of the vehicle from that date.

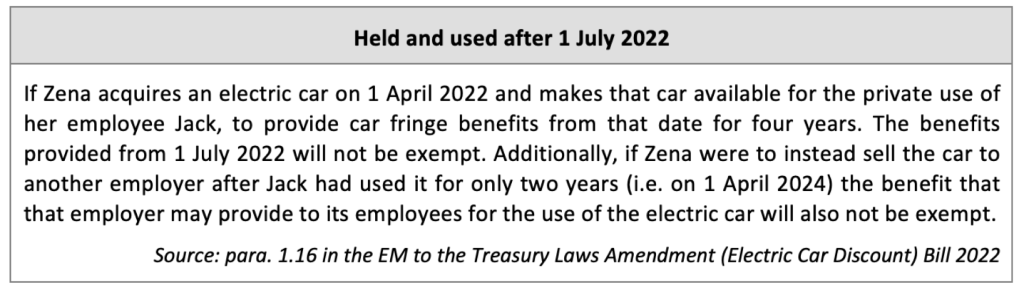

The exemption applies to a car benefit only if the earliest time when a person both held and used the car was at or after the start of 1 July 2022.

This involves two distinct tests:

The exemption will only apply if the first time that both of these tests are met is after 1 July 2022.

The FBT exemption extends to any associated benefit in running the eligible car for the period the car fringe benefit was provided, e.g. registration, insurance, repairs and maintenance, and fuel (including electricity).

![]() Note:

Note:

A home charging station is not a car expense associated with providing a car fringe benefit for electric cars. It may need to be considered as either property fringe benefit or an expense payment fringe benefit.

ATO webpage ‘Fringe benefits tax — Electric cars exemption’ (QC 71132)

TaxBanter’s online Monthly Special Topic to be held on 5 April 2023 is Using Cars. This session will provide an in-depth explanation of the exemption, including:

Register or learn more through the link below.

Join thousands of savvy Australian tax professionals and get our weekly newsletter.