[print-me]

Corporate clients are in the midst of finalising their 2016–17 financial statements, calculating tax liabilities and deciding how much of the year’s profits to pay out as dividends. This same process occurs each year … but it will not be business as usual this time!

The new suite of tax cuts and fundamental changes to how franking credits are calculated took effect on 1 July 2016 — but became law a mere six weeks before year end. Since the changes were enacted in May 2017, tax practitioners nationally have been seeking elusive guidance as to how these rules affect their clients.

From the 2001–02 to the 2014–15 income years, the tax rate for all companies in Australia (other than not-for-profits and life insurance companies) was 30 per cent.

The simplicity of a single-tier, flat rate system for the vast majority of corporate taxpayers did not last. As part of the Government’s package of initiatives to stimulate the small business sector, a concessional tax rate of 28.5 per cent for companies that were ‘small business entities’ (SBEs) — i.e. companies that carried on a business and whose aggregated turnover was less than $2 million — was implemented for the 2015–16 income year. This created a two-tier corporate tax system; non-SBE companies remained subject to the standard 30 per cent rate.

The concessional tax rate of 28.5 per cent lasted only one year. On 31 March 2017, after nearly a year of political debate, the Senate finally agreed to pass an amended version of that part of the Government’s proposed 10-year tax relief package (known as the Enterprise Tax Plan) which sought to reduce the corporate tax rate. The amended legislation received Royal Assent on 19 May 2017, but left the big end of town without a reduction in their corporate tax rate.

A second bill containing the remaining part of the corporate tax cuts for the big end of town (i.e. those companies with a turnover of $50 million or more) remains before Parliament.

The enacted legislation implements a series of tax cuts from the 2016–17 to the 2026–27 income years. In the first stage of the plan, companies that carry on a business and have an aggregated turnover of less than $10 million for 2016–17 are entitled to the concessional 27.5 per cent tax rate. This includes SBE companies that enjoyed the 28.5 per cent rate in 2015–16.

By 2026–27, all companies that carry on a business and have an aggregated turnover of less than $50 million will be taxed at 25 per cent — permanently.

So, for now, not only does Australia have a two-tier corporaten tax system, it will not be a static system: the parameters (i.e. the threshold and the concessional tax rate) will change many times over the next 10 years.

The first step in helping your clients is to work out which companies can access the concessional tax rate and which ones cannot … being mindful that this needs to be done every year, as a company may qualify for the lower tax rate for one income year but not for the next.

A company is eligible for the 27.5 per cent rate in 2016–17 where:

From 2017–18, a company is eligible for the concessional tax rate for a particular income year where:

Now that the standard 30 per cent rate does not automatically apply to all companies, we must carefully consider the following questions for every corporate client:

For the 2017–18 to the 2026–27 income years, this is the first question to be considered. Establishing the specific year is crucial as the tax rates and thresholds will regularly change over the next 10 years.

[fusion_table]

Aspect |

Changes between 2016–17 and 2026–27 |

|---|---|

| Type of eligible entity | In 2016–17, the company must be a SBE. From 2017–18, the company must be a ‘base rate entity’ (BRE) (see below). |

| Turnover threshold | The aggregated turnover threshold — which is one component of the SBE/BRE test — will progressively increase from $10 million in 2016–17 to $50 million in 2018–19. |

| Concessional tax rate | The concessional tax rate will progressively decrease from 27.5 per cent in 2016–17 to 25 per cent in 2026–27. |

[/fusion_table]

|

One component of the SBE/BRE test is that the company must have ‘carried on a business’ during the relevant year.

This is easy to satisfy where the company is actively trading. However, there is much conjecture as to whether a company ‘carries on a business’ for tax purposes if all or most of its income is derived from what would normally be characterised as ‘passive’ investment activities: interest, rent, dividends and trust distributions.

Recent developments have further muddied the waters for passive investment companies, such as holding companies and corporate beneficiaries of discretionary trusts.

On 15 March 2017, the ATO issued TR 2017/D2 which sets out the Commissioner’s preliminary views in relation to the central management and control limb of the corporate residency test for foreign incorporated companies. Footnote 3 to the draft ruling indicates that the ATO accepts that a passive investment company is likely to be ‘carrying on business’ for those purposes. Some commentators (making a quantum leap) have joined the dots and concluded that a passive investment company can access the concessional 27.5 per cent tax rate based on a broad interpretation of that footnote.

By early July 2017, the media had picked up the story, prompting the Government to counter-respond on 4 July 2017 with a media release adamantly declaring that the tax cuts were not meant to apply to passive investment companies. There has even been conjecture that the Government will implement a legislative amendment to tighten the meaning of what constitutes ‘carrying on a business’.

Unfortunately, this rumoured amendment did not transpire during the recent Parliamentary sittings. The ATO has also not yet clarified its position; so — for now — holding companies and corporate beneficiaries will have to continue to wait for much-needed clarification on which tax rate applies to them.

From 2017–18, the current year aggregated turnover is the other component of the BRE test. For that income year, a company that carries on business must also have an aggregated turnover of less than $25 million. The threshold increases to $50 million from 2018–19.

For 2016–17, the current year aggregated turnover is also used in the SBE test. However, for SBE purposes only, if the company’s 2016–17 turnover is not below $10 million, the turnover of the prior income year (i.e. 2015–16) is tested.

Remember that ‘aggregated turnover’:

Let’s deal with the second part of the question first. The prior year aggregated turnover may be relevant — if the income year in question is 2016–17 and access to the lower company tax rate of 27.5 per cent is determined by the company’s status as an SBE. This would be most of the corporate tax returns and accounts that are currently being prepared. A company (that carried on a business in 2016–17) is a SBE if either:

Therefore a company’s 2015–16 aggregated turnover is relevant in determining whether the company is eligible for the 27.5 per cent rate in 2016–17 — which will be the case if its 2016–17 turnover is, or is likely to be, at least $10 million.

Prior year aggregated turnover is not relevant for the 2017–18 and later income years. This is because the meaning of BRE has regard only to current year turnover.

Since the corporate tax cuts became law in May 2017, TaxBanter trainers have regularly been asked: Can I choose to pay tax at the higher rate (of 30 per cent) so that I can continue to frank my dividends at 30 per cent (rather than 27.5 per cent)?

The answer is a decisive No. Where the company satisfies all of the eligibility criteria for the concessional tax rate, it will be assessed at that rate. An eligible company cannot ‘choose’ to apply the lower rate in the same way that it can choose to utilise many of the small business concessions in Div 328.

For 2017 tax returns that are now being prepared, the ATO has offered administrative guidance in recognition of the confusion caused by the changes in the law late in the income year.

In any case, the premise of the question — while well-intentioned — is off-base: the rate at which profits of one income year are taxed does not guarantee the rate at which dividends paid out of those profits are franked in a later income year. The following section discusses this change in the fundamental mechanics of the imputation system.

Before 1 July 2016, the franking credits that could be attached to dividends represented the corporate tax paid on the underlying profits.

From 2016–17, the operation of the imputation system is based on the company’s corporate tax rate for the year in which the dividend is paid, worked out having regard to the company’s turnover for the previous income year.

This change has led to much consternation as company representatives and their tax advisers realise the impact of franking dividends at the lower rate of 27.5 per cent where the franking credits arose from tax paid at the higher rate of 30 per cent.

Many companies will end up with inaccessible franking credits permanently remaining in their franking accounts, because they cannot be passed out at more than the concessional rate for that year. As the corporate tax rate continues to decrease, so will the rate at which those franking credits can be passed out.

From an administrative perspective, the new franking rules have complicated what should be a routine dividend payment process.

Under the new franking rules, the franking rate is known as the ‘corporate tax rate for imputation purposes’.

Calculating the corporate tax rate for imputation purposes that applies to a particular dividend payment involves a two-step process:

| Step 1 | What was the aggregated turnover for the previous income year? |

| Step 2 | What is the tax rate that would apply in the current income year to the Step 1 turnover — based on the threshold for the current income year? |

The rate that results from Step 2 is the company’s corporate tax rate for imputation purposes for the year of the dividend payment.

| Example |

|---|

| Star Pty Ltd (Star) carried on business in 2015–16 and 2016–17. Its aggregated turnover in 2015–16 was $8 million. As it was not a SBE, it paid tax at 30 per cent (i.e. tax of $2.4 million).

During 2016–17, the directors of Star paid out the after-tax profits of $5.6 million. What is the correct franking rate?

Therefore the maximum franking rate for the dividend paid during 2016–17 is based on the rate of 27.5 per cent. It is not relevant that tax was paid on the underlying profit at the rate of 30 per cent. It is also irrelevant what Star’s 2016–17 aggregated turnover was and what tax rate applies for that year. The excess franking credits, representing the 2.5 per cent of profits paid as income tax, will remain trapped in Star’s franking account unless it can be attached to a distribution of untaxed income. |

Aside from the administrative complexity, the new franking rules will result in the following two general trends over the longer term:

Given that the legislative changes were not enacted until 19 May 2017, many companies that should have franked dividends in 2016–17 at 27.5 per cent had franked them at 30 per cent. Companies are not permitted to frank their dividends at 30 per cent where they should be franked at the 27.5 per cent rate, so on 22 May 2017 the ATO issued draft administrative guidelines to assist taxpayers to correct their franking with no penalty.

Unfortunately, this corrective action will impact on shareholders who relied on the 30 per cent franking credit previously advised by affected companies, and they may in fact have already lodged their 2017 returns which will necessitate amendment of their tax return in order to claim the correct franking credit.

The domino effect is an inevitability of which tax practitioners will have to be mindful.

All this trouble, all this fuss, all this complexity, all this confusion … for what should have been a simple reduction in the corporate tax rate for small business.

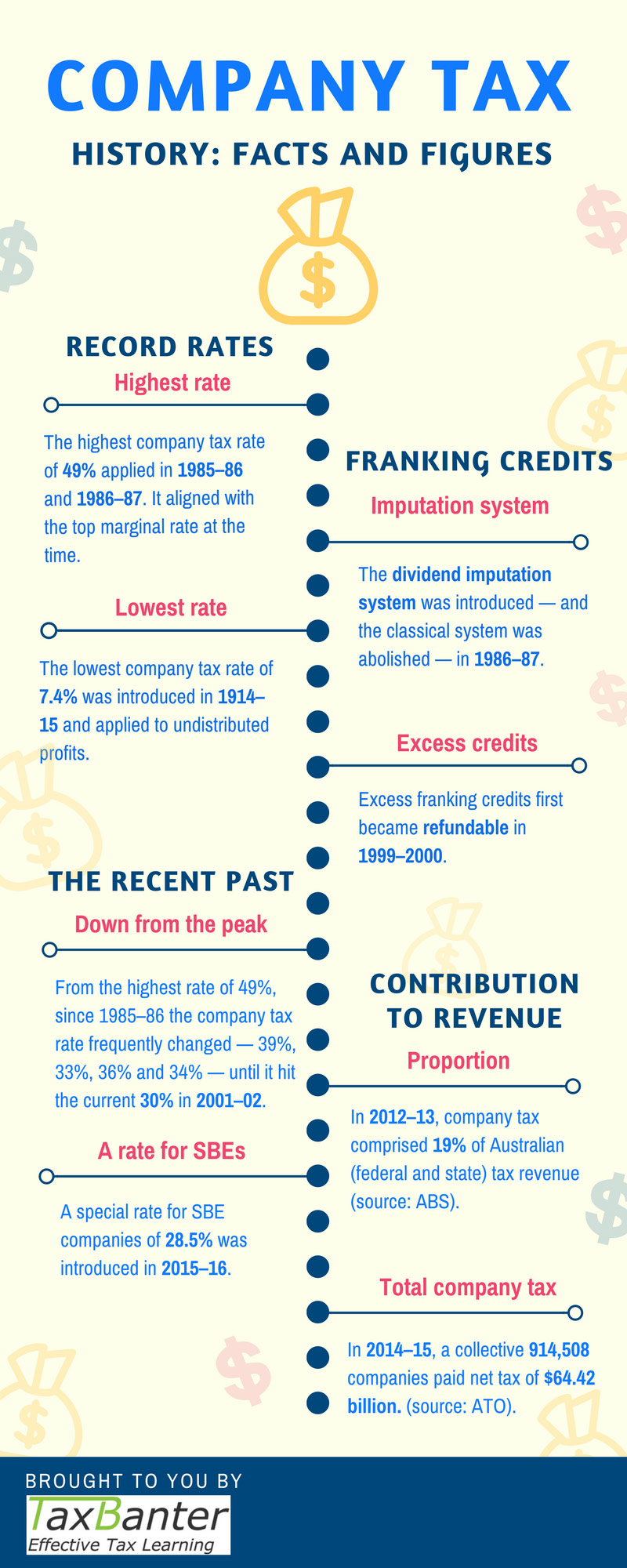

Click to see infographic: The history of Australia’s company tax and dividend imputation systems:

Contact TaxBanter to discuss your 2018 tax training needs: 03 9660 3500 | enquiries@taxbanter.com.au

Join thousands of savvy Australian tax professionals and get our weekly newsletter.

Definition

Definition