[lwptoc]

On the evening of Tuesday 29 March 2022, the Treasurer handed down the Federal Budget 2022–23. The Budget documents are available here.

On 31 March 2022, the Treasury Laws Amendment (Cost of Living Support and Other Measures) Bill 2022 (the Bill) received Royal Assent. The Bill amended the Tax laws to implement a number of Budget announcements (as summarised below).

The Excise Tariff Amendment (Cost of Living Support) Bill 2022 and the Customs Tariff Amendment (Cost of Living Support) Bill 2022 (the Fuel Excise Bills), which contain amendments to temporarily reduce fuel excise, also received Royal Assent on 31 March 2022.

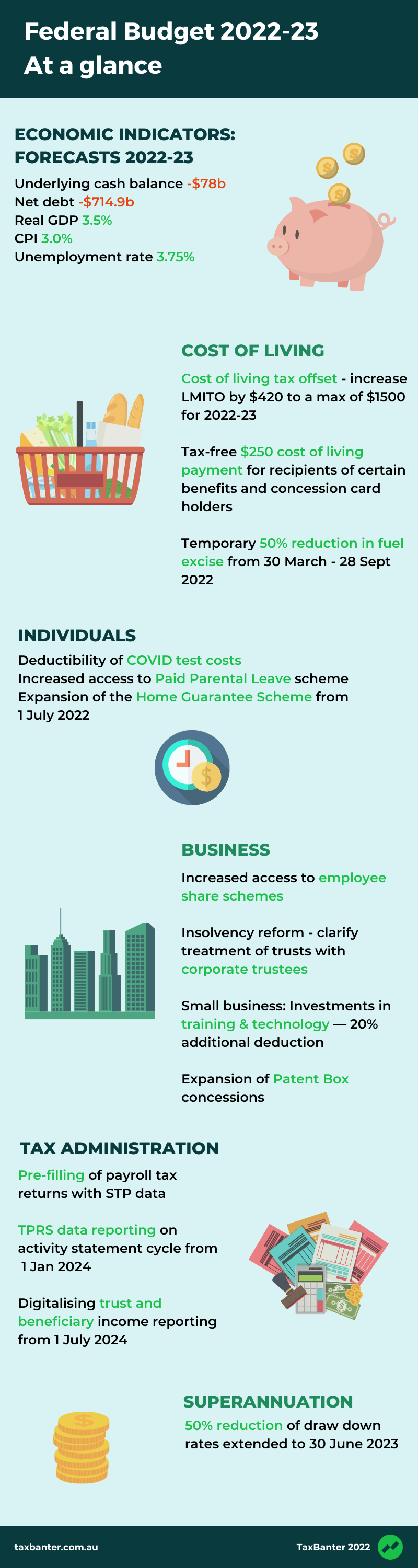

This pre-election Budget was positioned to assist individuals with the sharply rising cost of living. Australians have in particular experienced increasing bills at the supermarket and the bowser, the problem exacerbated by the worldwide COVID-19 pandemic, Australian floods and the Russia-Ukraine conflict all contributing to skyrocketing input and transport costs. National wage growth, forecasted to be 2.75 per cent for the 2022 financial year, is certainly not keeping up with the estimated CPI increase of 4.25 per cent for the year.

This cost of living relief will primarily come in the form of a $420 increase to the Low and Middle Income Tax Offset (LMITO) for this year, a one-off $250 bonus payment for social security support recipients and a six-month halving of the fuel excise. In addition, many soon-to-be new parents — including single parents — will benefit from the proposed enhancements to the Paid Parental Leave (PPL) scheme, which will broaden eligibility to more families and increase flexibility.

There are no big-ticket announcements for businesses, but eligible businesses may benefit from additional deductibility boosts for investments in technology and training, expanded access to employee share schemes, increased support for apprenticeships and a number of improvements to the tax compliance experience.

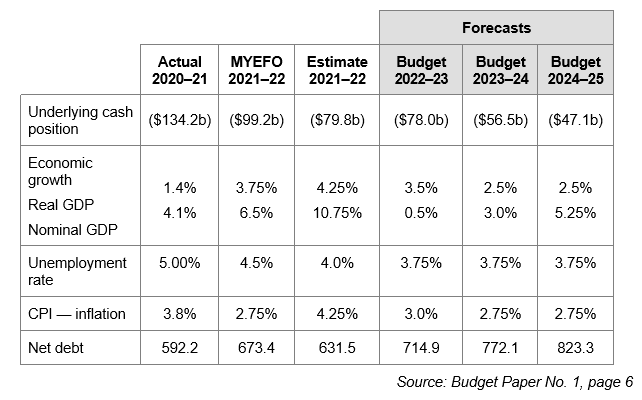

The key economic forecasts in the Budget papers include:

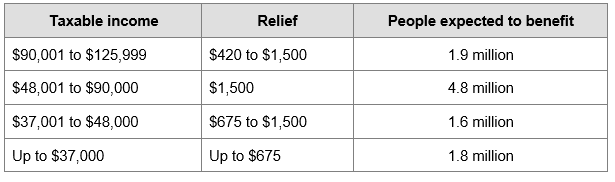

Schedule 6 to the Bill introduces amendments to increase the LMITO by $420 for the 2021–22 income year. This consequentially increases the maximum LMITO benefit to $1,500 (previously $1,080).

Unless the full offset is required to reduce a taxpayer’s tax liability to zero, all LMITO recipients will benefit from the full $420 increase. All other features of the LMITO remain unchanged, including the requirement that relevant income is below $126,000.

Consistent with current arrangements, the LMITO will be received on assessment after the individual lodges their 2022 tax return.

Note

Note

The 2021–22 income year is the final year of the LMITO. All else being equal, recipients of the increased LMITO this year will face a higher tax bill for the 2022–23 income year. The Stage 3 tax cuts are legislated to begin in 2024–25.

Schedule 8 to the Bill introduces the new 2022 cost of living payment. Under this measure, the Government will provide eligible recipients with a one-off, tax-exempt support payment of $250 to assist with higher cost of living pressures.

The payment will be made to eligible concession card holders and recipients of the following payments:

Recipients must be residing in Australia, and have been receiving one of the qualifying payments or held or had clalimed and qualified for one of the qualifying concession cards on 29 March 2022.

The payments will not count as income support for the purposes of any income support payment. A person can only receive one economic support payment, even if qualify under multiple categories.

The $250 will be paid automatically to eligible recipients in April 2022.

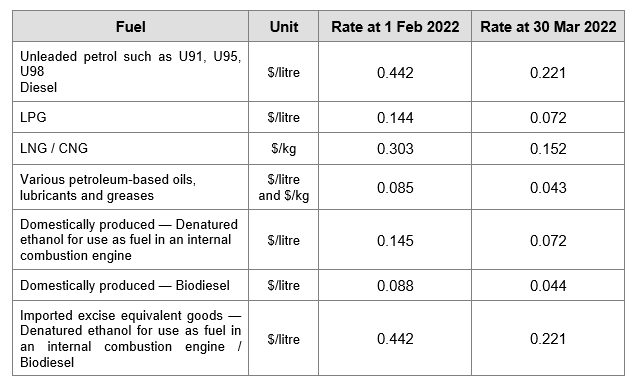

The Fuel Excise Bills enable temporary relief from fuel price pressures by halving the excise and excise-equivalent customs duty rate that applies to petrol and diesel for six months.

The 50 per cent reduction will apply to the excise and excise-equivalent rates that apply to:

for six months from 12.01 am on 30 March 2022 until 11.59 pm on 28 September 2022.

The impact of the halving of the excise rates and excise equivalent goods customs duty rates is set out in the table below:

The impact of the halving of the excise rates and excise equivalent goods customs duty rates is set out in the table below:

Existing policy settings for fuel excise and excise-equivalent customs duty, including indexation in August, will continue but on the basis of the halved rates.

The excise and excise-equivalent customs duty rates will, at the end of the six-month period, revert to previous rates including indexation that would have occurred on those rates during the six-month period.

The Australian Competition and Consumer Commission (ACCC) will monitor the price behaviour of retailers to ensure that the lower excise rate is fully passed on to Australians.

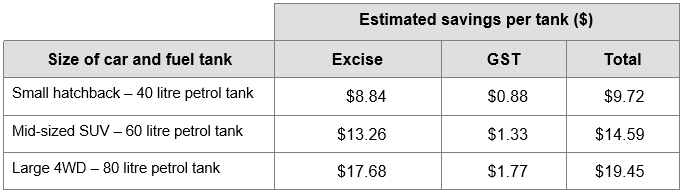

Household savings in excise and GST per tank of fuel are estimated to be as follows:

Eligible businesses receive fuel tax credits (FTC) for the excise that is included in the price of fuel. The rate of the FTC depends on the size of the vehicle and where it is used. Heavy vehicles travelling on public roads have their FTC reduced by the road user charge (RUC).

The Government is not changing the existing RUC arrangements for heavy vehicles travelling on public roads, but the temporary reduction in fuel excise will provide a net benefit for heavy vehicle operators of 4.3 cents per litre from 30 March 2022, compared to current settings.

In the Federal Budget, the Government announced that:

Schedule 2 to the Bill introduces new s. 25-125 into the ITAA 1997. Under the new provision, an individual may deduct a loss or outgoing to the extent it is incurred in gaining or producing their assessable income if:

Section 25-125(3) specifies a test covered by the provision is a test that is:

The Bill does not amend the FBTA Act to provide a separate FBT exemption for COVID-19 testing costs incurred by employers. Instead, from 1 July 2021 employers may apply the otherwise deductible rule to reduce the taxable value of fringe benefits related to the provision of COVID-19 tests for the benefit of employees, or the reimbursements of testing costs incurred by employees.

![]() Implications

Implications

Ancillary costs of acquiring the tests, such as the cost of travelling and parking to purchase a test will not be deductible, however it is not the policy intention to exclude other incidental costs such as vendor credit card surcharge fees and postage and handling for online purchases.

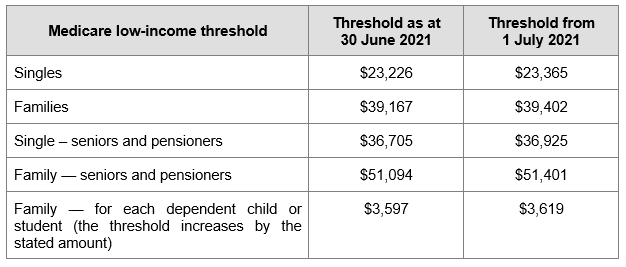

Schedule 1 to the Bill increases the Medicare levy low-income threshold for singles, families, and seniors and pensioners, and the Medicare levy surcharge low-income threshold, from 1 July 2021:

Schedule 4 to the Bill introduces legislative changes to ensure that participants of employee share schemes (ESS) in unlisted companies will be allowed to invest up to:

Regulatory relief from the Corporations Act 2001 is also extended to offers to independent contractors, where they do not have to pay for the interests.

The amendments will commence six months after Royal Assent.

Schedule 5 to the Bill varies the GDP uplift factor for PAYG and GST instalments at two per cent in respect of instalments that relate to the 2022–23 income year. The lower uplift rate will provide cash flow support to small businesses including sole traders and other individuals with investment income.

The two per cent GDP uplift rate — rather than the statutory 10 per cent — will apply to small to medium enterprises which have aggregated turnover of up to:

Other Federal Budget announcements which have not yet been legislated include the following.

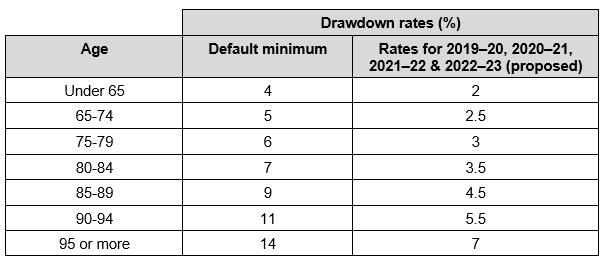

The Government will extend the 50 per cent temporary reduction of the superannuation minimum drawdown requirements for account-based pensions and similar products for a further year to 30 June 2023.

The Government will broaden the availability and scope of the existing Home Guarantee Scheme by:

The Government will introduce the Enhanced Paid Parental Leave (Enhanced PPL) scheme. Proposed changes to the current PPL scheme include:

The Government intends to introduce the changes to the PPL no later than 1 March 2023.

This measure forms part of the $2.1 billion investment package in the Women’s Budget Statement.

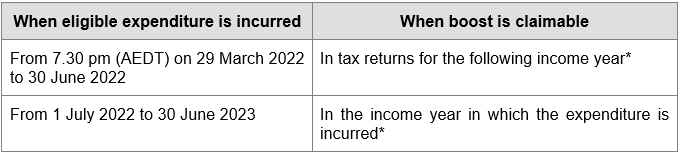

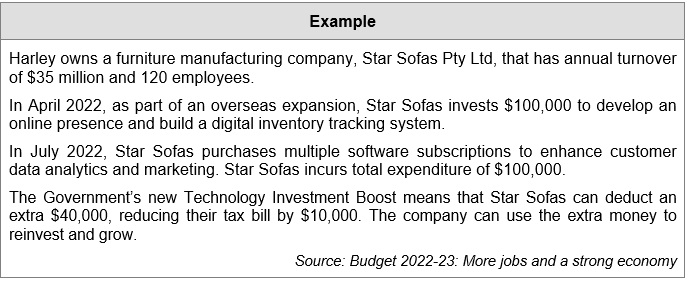

The Government announced that it is introducing a technology investment boost to support digital adoption by small businesses.

Small businesses (with aggregated annual turnover of less than $50 million) will be able to deduct an additional 20 per cent of expenditure incurred on business expenses and depreciating assets that support their digital adoption, such as portable payment devices, cyber security systems or subscriptions to cloud‑based services.

An annual cap will apply in each qualifying income year so that expenditure up to $100,000 will be eligible for the boost.

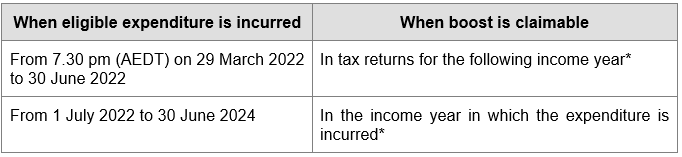

The 20 per cent boost will be claimable as follows:

* This may not be the 2023 tax return if the business is a Substituted Accounting Period taxpayer.

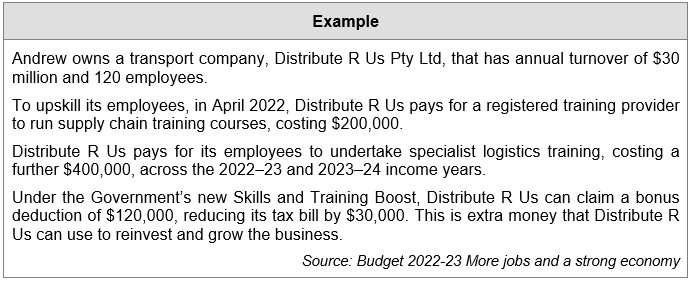

The Government announced that it is introducing a skills and training boost to support small businesses to train and upskill their employees.

Small businesses (with aggregated annual turnover of less than $50 million) will be able to deduct an additional 20 per cent of expenditure incurred on external training courses provided to their employees. The external training courses will need to be provided to employees in Australia or online and delivered by entities registered in Australia.

Some exclusions will apply, such as for in‑house or on‑the‑job training and expenditure on external training courses for persons other than employees.

The 20 per cent boost will be claimable as follows:

* This may not be the 2023 or 2024 tax return if the business is a Substituted Accounting Period taxpayer.

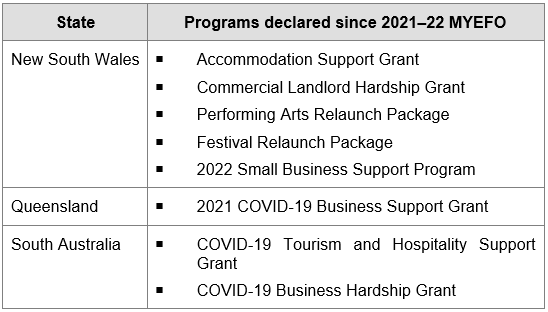

The Government announced that it will extend the measure which enables payments from certain state and territory COVID‑19 business support programs to be made non‑assessable non‑exempt (NANE) for income tax purposes until 30 June 2022 (extended from 30 June 2021). This extension was passed into law in June 2021.

In the Budget the Government announced that the following State grant programs have been declared eligible for NANE treatment since the 2021–22 MYEFO:

The Government has announced that it will provide additional funding to further reform insolvency arrangements, including:

The Government has announced that it will expand the Patent Box regime to:

For the agricultural sector and low emissions technology innovations, eligible corporate income will be subject to an effective tax rate of 17 per cent in relation to rights and patents granted after 29 March 2022 and for income years starting on or after 1 July 2023.

The Government will support employers to engage and retain new apprentices and reform the Australian Apprenticeships system by:

The Government has announced a suite of proposed measures intended to improve the tax compliance and administration experience for businesses:

The Government has announced that — subject to software providers being able to have systems in place — businesses will have the option to report Taxable Payments Reporting System data (via accounting software) on the same lodgment cycle as their activity statements.

It is anticipated that systems will be in place by 31 December 2023, with the measure to commence on 1 January 2024, for application to periods starting on or after that date.

Currently a Taxable Payments Annual Report must be lodged by 28 August each year.

Currently, ABN holders are able to retain their ABN regardless of whether they are meeting their obligations to lodge income tax returns, or to update their ABN details on the Australian Business Register.

As part of the 2019–20 Federal Budget, the Government announced that it would strengthen the ABN system to disrupt Black Economy behaviour.

The Government has announced that it will defer the start date of this measure by 12 months to assist with integration into the Australian Business Registry Services.

As a result:

The Government will provide companies with the option of having their PAYG instalments calculated based on current financial performance, extracted from their business accounting software, subject to some tax adjustments.

The measure proposes to leverage from a company’s electronic reporting systems to improve the alignment between PAYG instalment liabilities and profitability. The measure should also reduce compliance costs, improve processing times and support cash flow management for SMEs (for example the measure may enable a company to automatically receive refunds of instalments paid if financial performance declines).

The measure is proposed to commence on 1 January 2024 for periods starting on or after that date — subject to software providers’ capacity to deliver operational systems by 31 December 2023.

The Government will commit $6.6 million towards the development of IT infrastructure required to allow the ATO to share Single Touch Payroll (STP) data with State and Territory Revenue Offices on an ongoing basis, following further consideration of which States and Territories are able and willing to make investments in their own systems and administrative processes to pre-fill payroll tax returns with STP data, to reduce compliance costs for businesses.

The Government will digitalise trust and beneficiary income reporting and processing, by allowing all trust tax returns to be lodged electronically. This will allow greater pre-filling and automating of ATO assurance processes.

As trust income reporting and assessment calculation processes have not been automated to the same extent as individual or company tax returns, there are longer processing times and limited pre‑filling opportunities. This measure, by facilitating the electronic lodgment for up to 30,000 trusts that currently lodge by paper, will reduce the compliance burdens on taxpayers, reduce processing times and enhance ATO processes.

Note

Currently trust tax returns for large managed investment trusts or public unit trusts are excluded from electronic lodgment.

You can view the full resolution/size here.

A recording of our 2022-23 Federal Budget webinar can be purchased here.

Our upcoming Tax Updates will cover the recently passed Budget legislative package, as well as the yet to be legislated Budget announcements. You can view our upcoming April sessions through our Public Sessions page (face-to-face sessions – choose location, then month), or alternatively you can join our April Online Tax Update.

Have a group of 5 or more on your team? Check out our in-house training option, which is the most cost effective options for larger groups. One of our Senior Tax Trainers will come to your firm and deliver a tailored session specifically for your staff and client base.

Our mission is to offer flexible, practical and modern tax training across Australia – you can view all of our services by clicking here.

Join thousands of savvy Australian tax professionals and get our weekly newsletter.